NERC president warns of ‘five-alarm fire’ for grid reliability

“The reliability of the power grid remains extremely high, but ... the risks to reliability continue to mount,” the North American Electric Reliability Corp.’s Jim Robb told federal regulators.

By: Ethan Howland• Published Oct. 22, 2025

The issue of data centers — and how to ensure they can be safely added to the grid — was a key focus of a grid reliability conference held by the Federal Energy Regulatory Commission on Tuesday.

Generally, grid reliability is strong in the United States, but challenges are growing, Jim Robb, president and CEO of the North American Electric Reliability Corp., said at the meeting.

“The reliability of the power grid remains extremely high, but, paradoxically, the risks to reliability continue to mount,” Robb said. “We're seeing … an increasing number of small scale events and near misses that continue to reinforce what we can't call anything but a five-alarm fire when it comes to reliability.”

According to Robb, grid reliability challenges include dwindling resource adequacy with weakening reliability services, extreme weather, interdependency with natural gas and other sectors, especially telecommunications, policies affecting resource and fuel development, load development, the ability to site and permit needed infrastructure and an “escalating toxic soup” of physical and cybersecurity risks.

The U.S. faces potential imbalances between electricity supply and demand amid uncertainty about how much load may be coming online and how much generation and transmission must be built to handle it, saidFERC Commissioner Judy Chang, warning that the risks and uncertainties around those issues are “coming to a head.”

Estimates in data center growth range widely. The U.S. Department of Energy in December said U.S. data centers could use 6.7% to 12% of all U.S. electricity by 2028, up from 4.4% in 2023.

The U.S. needs to build energy infrastructure more quickly, according to FERC Chairman David Rosner.

“I see our grid as needing every single megawatt, every single electron and every single molecule we can get to meet demand on those peak days and peak hours,” Rosner said. “That means we need to make sure that we're studying faster, we're giving permits faster and unlocking all different types of energy infrastructure that are needed.”

The power sector needs to move quickly to address reliability challenges, according to Jennifer Curran, senior vice president of planning and operations for the Midcontinent Independent System Operator.

“Where we are today, I would say, is not safe because we are in a tight reserve margin situation,” Curran said. “We are in a situation where we do have new types of resources coming on, and we are going to have to make our best steps to continue to increase reliability.”

Given the uncertainty, Curran called for ensuring the grid system has adequate “shock absorbers,” such as improved data analysis tools.

“How do we make sure that we have both in our physical grid and in our market products … the right incentives to make sure that we are able to bear these uncertainties that are really going to be coming before us?” Curran asked.

“The best thing we can do is get better at quickly dealing with the uncertainty and having as much built-in infrastructure as we can to really provide that balance of reliability and economic efficiency,” she continued. “Getting the transmission built to help provide those connections and provide that optionality within the system is something that's really important, and it takes a long time.”

Electricity affordability and the grid buildout

Dealing with some of those challenges will be costly, according to FERC Commissioner Lindsay See.

“Some of that is inevitable, but we are reaching a point where bills are becoming incredibly difficult for people across the country,” See said.

Some states are taking measures to try and shield ratepayers from costs associated with data centers and other large loads.

Tricia Pridemore, a commissioner at the Georgia Public Service Commission, said with appropriate guardrails, large data centers can help reduce electric rates.

In Georgia, large loads enter into 15-year contracts to pay for all the new generation, transmission and distribution needed to manage their load, Pridemore said. The PSC recently approved a plan for Georgia Power to add 7.1 GW of capacity to meet growing demand, which the commission estimates will reduce residential rates by $2.64 a month, she said.

Matthew Holtz, vice president of transmission operations at Invenergy, said merchant transmission, which is paid for by entities buying capacity of transmission lines, can take cost burdens off ratepayers.

Invenergy is also calling for “cloud-based” system monitoring, which Holtz said could lead to more economic energy and capacity sharing between regions and help respond to extreme weather events.

Long-term and more integrated system planning that co-optimizes transmission, generation and load solutions could put downward pressure on electric rates, according to Carlos Casablanca, managing director ofdistribution planning and analysis at American Electric Power.

“We are seeing … a lot more costs coming: the build out that needs to occur to accommodate large loads, and also the resources that are required to both address retiring generation but also meet the need from the large loads,” Casablanca said. “So anything we can do in the planning space to prepare for what's coming and optimize as early as we can, it'll help. It'll pay dividends down the road.”

US electric utilities entering investment ‘super-cycle'

Electric utilities will spend $1.4 trillion from 2025 to 2030, the firm said. They face challenges around data center demand forecasting, rising rates and regulatory lag.

By: Robert Walton• Published Oct. 27, 2025

U.S. electric utilities are entering a five-year capital expenditure “super-cycle” as they build out transmission and generation networks to meet new demand from data centers, Morningstar DBRS said in a Monday research note.

“Investment in electricity infrastructure is projected to be $1.4 trillion from 2025 to 2030, double the amount invested in the prior 10 years,” the firm said. And based on data from the North American Electric Reliability Corp., Morningstar said many regions can expect load growth to increase from previously estimated 6.1% to around 11.6% over the next decade.

“The challenges posed by the rapid buildout of data centers are overlaid on existing concerns for most utilities, including decarbonization and guaranteeing the reliability of grid infrastructure while increasing the contribution of renewable power,” Morningstar said. “The projected surge in demand provides opportunities for utilities that must be counterbalanced with structural changes and regulatory support for utilities and rate payers.”

"We anticipate that regulated utilities with supportive regulatory commissions, solid credit ratings, and access to capital markets will deploy the needed capex to take advantage of the data center boom," Bukola Folashakin, Morningstar assistant vice president of corporate ratings, said in a statement. "We expect this capex investment in turn to make such utility locations attractive for more data center construction, potentially creating a cycle of increased revenue for as long as data centers remain economically viable."

Some states — Morningstar named California, Texas, and Louisiana — will see elevated risks of resource inadequacy next year that “in extreme conditions, could trigger electricity shortfalls,” according to the note.

Morningstar’s analysis mirror’s recent capital expenditure estimates from the Edison Electric Institute, which expects U.S electricity generation to grow “for the foreseeable future.” The group, which represents investor-owned utilities, said generation rose 3% in 2024 and generation investments as a share of the industry’s total capital expenditures have risen for four straight years.

The rapid rise in electricity demand, following decades of stagnation, will challenge utilities in a few ways, according to Morningstar.

Uncertainty around needed data center capacity “makes it challenging for utilities to accurately forecast future power demand and the required investment,” according to the report. And those data centers bring demand surges that are driving “higher tolls for other customer segments,” which “will be exacerbated as more data centers become operational.”

Meeting the demand requires massive utility investment but “traditional funding sources are inadequate to meet future investment needs,” Morningstar said. “Utilities are increasingly looking to private capital to fill funding gaps,” while increased ratepayer-funded investments lead to regulatory lag.

Article top image credit: Courtesy of Public Service Electric and Gas

Grid planners and experts on why markets keep choosing renewables

Thinking of resources as either intermittent or backup oversimplifies the complexity of the grid, they said.

By: Herman K. Trabish• Published Oct. 9, 2025

As electricity demand grows, alongside wind and solar’s share in the U.S. energy mix, concerns about renewables’ reliability are being raised more frequently — including at the highest levels of the federal government.

“With the electricity grid, you have to match supply and demand in every moment in time,” Energy Secretary Chris Wright said recently on Fox News. “With wind and solar, you don’t know when they’re going to be there, and you don’t know when they’re going to go away.”

Wright went on to say the development of renewables has led to an “extra distribution grid” that has raised energy prices.

But utility planners, grid operators and analysts say wind, solar and batteries are an important part of an evolving power system in which intermittent resources can be reliably scheduled and called upon using sophisticated software and other tools.

They also point to both the levelized cost of electricity for renewables and their competitiveness in automated energy markets that select the least cost units to run in each hour.

“System operators don't decide whether resources bidding into the market are good or bad,” said Rob Gramlich, president of energy sector consultant Grid Strategies, in an interview.

“There is no central decision maker,” he said. “Markets don't play favorites.”

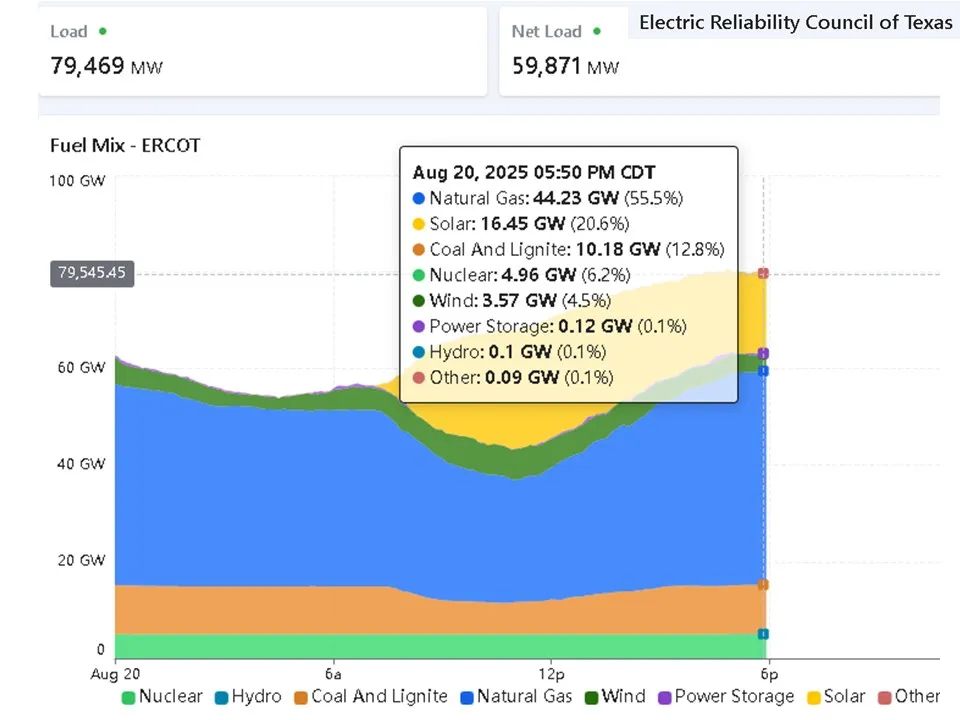

ERCOT’s multi-resource price-selected portfolio for Aug. 20, 2025, at 5:50 PM CDT

ERCOT "dashboard" [jpg]. Retrieved from dashboard.

With generators retiring, demand rising, and construction, financing, permitting and supply chain challenges growing, operators and analysts acknowledged concerns over the future of the U.S. power system. Many called for diversification of resources, including renewables and storage, to protect electricity reliability and affordability.

“The objective of planning is a portfolio of diverse resources at the least cost possible to avoid outsized impacts from any single one,” said Michael Eugenis, Arizona Public Service’s director of resource planning.

APS is pursuing renewables alongside more natural gas to maintain reliability in its territory, he said.

“That is not the same as a second set or a shadow set of resources,” he added.

Automated markets are selecting renewables

One of the major concerns cited by Wright and others is the intermittent nature of renewables and the impact of that on grid reliability.

One of the ways grid operators measure reliability is using a metric called effective load carrying capability, or ELCC.

ELCC is a complex calculation based on comparing what portion of a resource's nameplate capacity it produces on average in simulations of decades that include factors that cause it to vary, like performance, supply and demand. For fossil resources, variabilities are caused by things like maintenance outages and fuel supply issues. Weather variations impact wind and solar.

ELCCs vary by region and by each system’s portfolio makeup, but nuclear power generally has the highest ELCC, meaning on average over the years, it produces the closest percentage of its nameplate capacity.

Fixed-tilt solar had the lowest at 8%, and tracking solar was 11%. Onshore wind was 41%, offshore was 69%; storage was between 50% and 72%; gas was between 60% and 78%, and coal was 83%.

“System operators don't decide whether resources bidding into the market are good or bad ... Markets don't play favorites.”

Rob Gramlich

president of Grid Strategies

But despite their relatively low ELCCs, automated markets are consistently choosing renewables over other resources because they are cheaper at the time the grid needs them.

“The automated market mechanisms use all the relevant variables that affect load to pick the cheapest resources,” said Richard Doying, Grid Strategies vice president and a former executive vice president for market and grid strategy for the Midcontinent Independent System Operator.

Those resources are bid out, and “then the next cheapest resources, and so on,” Doying said.

“The markets are selecting wind and solar despite their low ELCCs and low capacity values because the return justifies the investment,” he added.

When they are both generating at the same time, renewables are often cheaper than fossil fuel power.

One reason for this is that the fuel and maintenance costs for fossil-based resources are significant, continuous and volatile. Natural gas prices, for example, have nearly doubled since 2024, but are still lower than they were in 2022 following Russia’s invasion of Ukraine.

The fuels for wind and solar are cost-free, maintenance outage costs are significantly less, and the capital expenditures to build projects are typically amortized over 20 years.

“If natural gas was the cheapest option to meet the peak, the markets would select it,” said Sean Kelly, co-founder and CEO of forecast provider Amperon and a former energy analyst.

When the sun’s not shining

Kelly said today’s advanced load and weather forecasting enhances the reliability of a resource portfolio with a high renewables penetration.

While good forecasting can alleviate much of the need for backup generation, he said, rising demand for power will likely require more firm generation to fill the gaps when there is no sun or wind.

The ability to choose the cheapest available power source in real time is why grid operators say renewables are an important part of the same, increasingly flexible power system — not a separate system.

“We don't have different systems; we have a portfolio of resources and capabilities that meet the needs of the system,” said Mark Rothleder, senior vice president and COO for the California Independent System Operator, in an interview.

California has one of the highest renewables penetrations in the United States. California also has some of the highest electricity rates. Some observers link those to things to argue that renewables drive up energy costs.

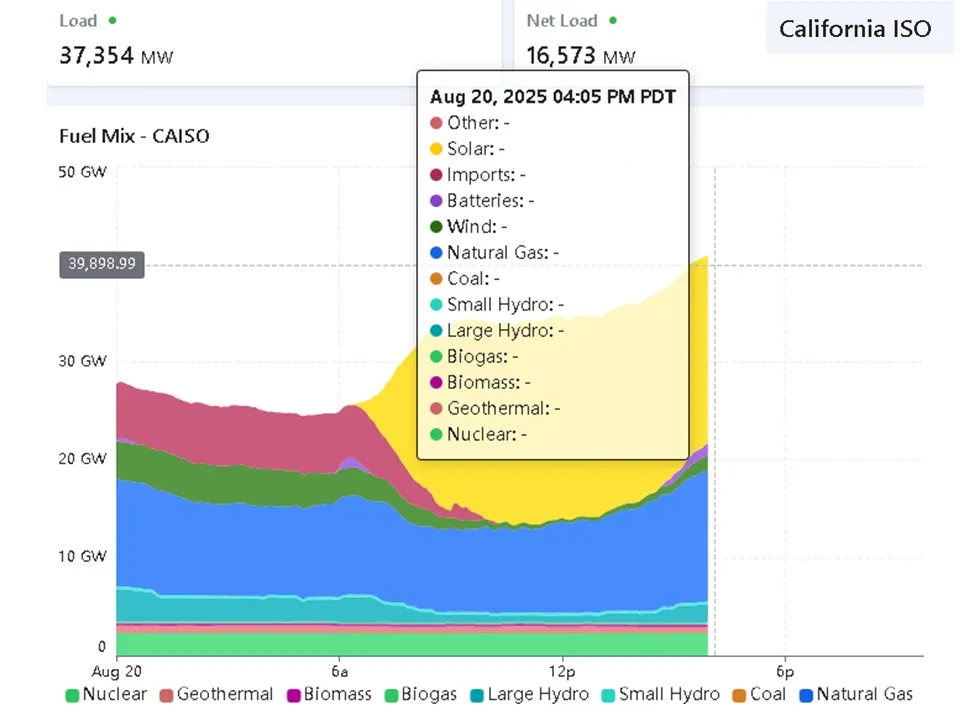

CAISO’s multi-resource price-selected portfolio for August 20, 2025, at 4:05 PM PDT

CAISO. (2025). "dashboard" [jpg]. Retrieved from dashboard.

But other states with high levels of renewable power have comparatively low rates compared to the national average.

In Iowa, for example, wind turbines generated 59% of the state’s electricity in 2023, according to the U.S. Energy Information Administration. Iowa was also in the 10 states with the lowest average electricity price that year.

While solar and wind are not always available locally when demand is high, storage penetrations are rising and some states are moving toward more regional energy markets where cheaply-produced energy from renewables can be more easily traded across state boundaries.

The New York Independent System Operator said in a recent report that although “duration-limited” generators like wind and solar require standby resources when the availability of the renewable fleet diminishes, “no generating type operates at full power, full time.”

Thinking of resources as either intermittent or backup oversimplifies the complexity of the grid, experts said.

“Wind and solar don’t have to produce 100% of the time because people aren't consuming all available electricity 100% of the time,” said Beth Garza, asenior fellow at the R Street Institute think tank and former ERCOT market monitor CEO.

“It is easy to vilify solar and wind,” Garza said. But regardless of the resource mix, “the average electricity load is only about half the peak demand.”

When demand peaks

Power systems have long been required to have reserve margins over the highest expected peak demand, and the growth of wind and solar has not changed that, said Julia Matevosyan, anassociate director and chief engineer with the Energy Systems Integration Group and a former ERCOT planning engineer.

But advancements in software and market shifts have democratized incentives for energy production, conservation and storage in ways that can smooth demand peaks and deploy resources as needed.

This flexibility can optimize wind, solar and batteries to deliver low cost electricity more reliably than “a more limited set of traditional resources,” Matevosyan said.

Over the summer, California deployed what some advocates have called the largest virtual power plant in the world when several aggregators discharged 539 MW of average output from more than 100,000 customer-sited batteries during peak demandbetween 7 and 9 p.m.

A Brattle Group study of the deployment commissioned by Sunrun and Tesla Energy, both of which participated in the VPP program, concluded that it could reduce the need for gas peaker plants and potentially save ratepayers $206 million between 2025 and 2028.

Ryan Hledik, one of the report’s authors, said the VPP makes better use of assets that have already been deployed.

“There are a growing number of examples of VPPs scaling faster and at a lower cost than conventional resources,” Hledik said.

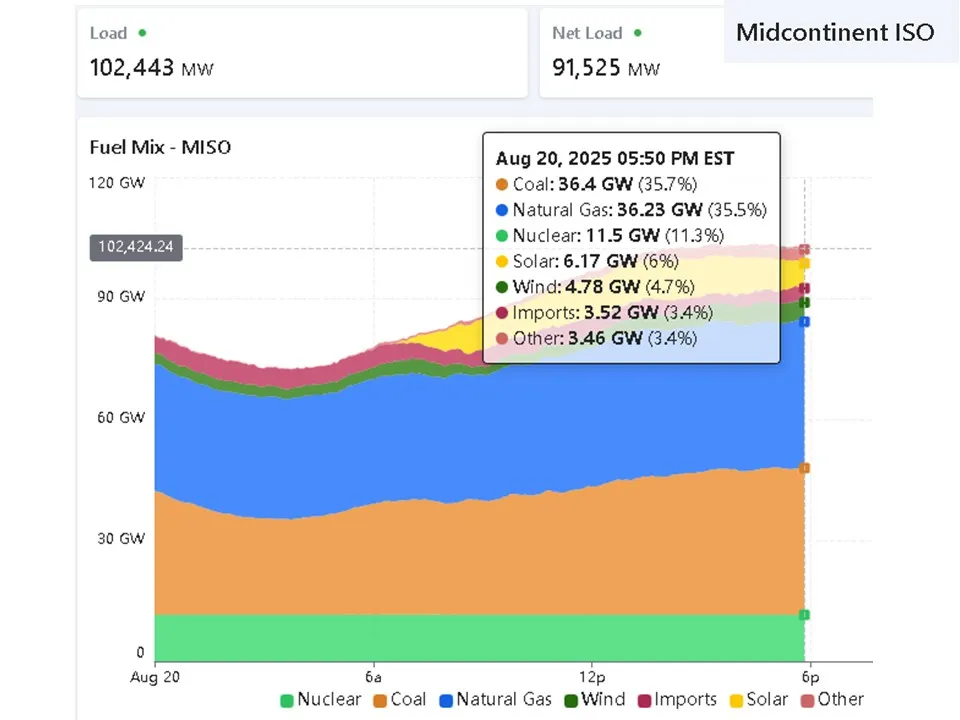

MISO’s multi-resource price-selected portfolio for August 20, 2025, at 5:50 PM EST

MISO. (2025). "dashboard" [jpg]. Retrieved from dashboard.

Renewables continue to dominate new generation as demand rises

Demand is rising for the first time in two decades. Last year, the U.S. used more electricity than ever before, and the EIA projects demand to grow more than 2% per year until at least 2026. Farther out, the predictions vary widely and are highly dependent on the growth of data centers, electrification and manufacturing.

The vast majority of new generation resources coming online now are renewable, with solar in the lead, followed by wind. In the first seven months of 2025, solar accounted for over 16 GW of the 21.5 GW added to the U.S. power system. Wind accounted for almost 3.3 GW and natural gas for 2.2 GW, the September Federal Energy Regulatory Commission Infrastructure Update reported.

Federal tax credits and other incentives that are being phased out boosted renewable development. But experts say even without that support, the economics are also in renewables’ favor.

“Wind and solar don’t have to produce 100% of the time because people aren't consuming all available electricity 100% of the time.”

Beth Garza

senior fellow at R Street Institute and former ERCOT market monitor CEO.

The levelized cost of electricity for utility-scale solar and onshore wind remain “the most cost-effective forms of new-build energy generation on an unsubsidized basis,” according to Lazard analysis. Calculating a technology’s LCOE involves its capital cost, fuel cost, capacity factor, and other values that vary by location and time.

Recently, renewable trade groups have warned of a slowdown in the solar industry. But alternative resources, like natural gas, face their own challenges, from lengthy planning and approval processes to rising fuel prices and years-long equipment backlogs.

“The newest, most efficient natural gas peaker plants are expensive to build and are likely to become more expensive to run because of competition for natural gas,” Garza said. “The market’s answer to load growth is still to build more wind, solar, and batteries because they are the cheaper and faster to build.”

Michelle Solomon, a manager of electricity policy at Energy Innovation, offered a similar observation.

Utilityplanning models “have largely been choosing wind and solar and batteries for several years,” she said. “A diverse set of resources is most likely to be the cheapest portfolio.”

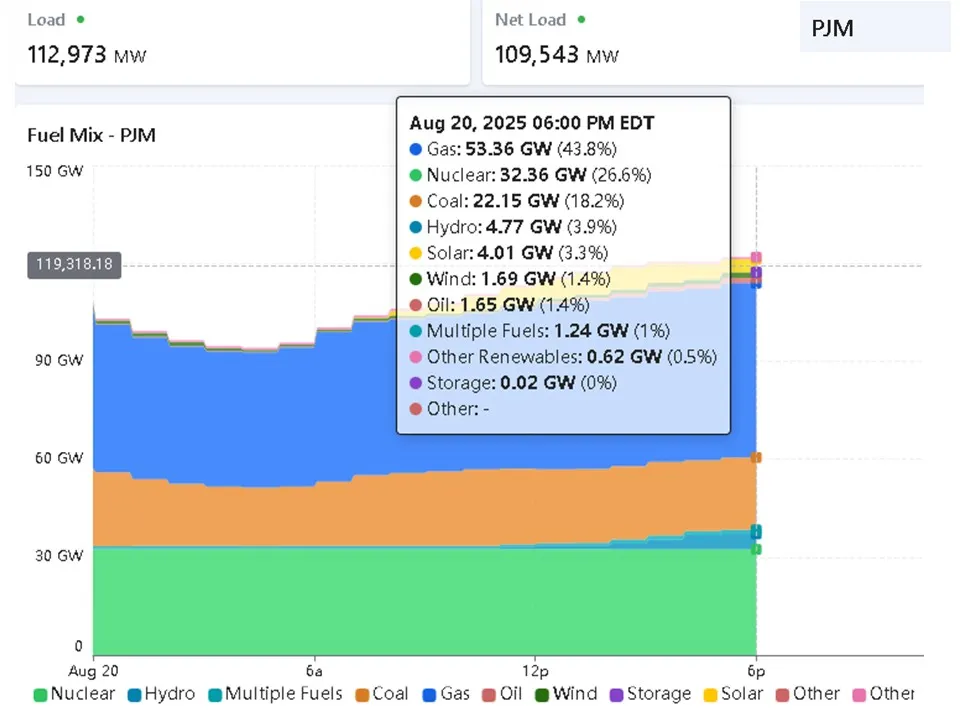

PJM’s multi-resource price-selected portfolio for August 20, 2025, at 6:00 PM EDT

PJM. (2025). "dashboard" [jpg]. Retrieved from dashboard.

Article top image credit: Anna Moneymaker via Getty Images

DOE large load interconnection proposal sparks federal-state jurisdiction concerns

State regulators, lawmakers and ratepayer advocates voiced alarm over the department’s interconnection proposal, while the Data Center Coalition offered qualified support.

By: Ethan Howland• Published Nov. 24, 2025

The U.S. Department of Energy’s proposal for federal regulators to set rules for interconnecting data centers and other large loads to the transmission system has sparked major jurisdictional concerns, according to filings at the Federal Energy Regulatory Commission.

FERC has never asserted jurisdiction over end-user load interconnections, NARUC said in response to a request for comments on the DOE’s request that the commission set rules for interconnecting large loads.

“The reason for this fact is that FERC asserting jurisdiction over load interconnection is outside the boundaries” of the FPA, NARUC said.

Also, states are responsible for determining rates for different customer classes, NARUC noted.

“If FERC were to assert jurisdiction over a service to a limited class of retail customers, it would interfere with the balancing performed by state regulators in retail rate cases, a determination that is solely a state decision,” said the group, which represents state utility regulators.

State lawmakers also raised concerns about DOE’s proposal.

“If jurisdiction for interconnection of large loads is claimed by the FERC, what is the process for determining how those large loads will impact an already strained power supply, and who bears responsibility for managing and mitigating the ensuing reliability concerns?” the National Conference of State Legislatures asked.

DOE’s proposal directing FERC to set standardized large-load interconnection rules includes 14 “principles”, including that new loads and co-located “hybrid” loads be responsible for all network upgrade costs that they cause. Also, reliability studies should be conducted when an existing power plant seeks to serve a new large load, according to DOE’s proposal.

About 150 comments were filed on the DOE’s proposal on Friday at FERC. Many appeared critical of expanding FERC’s role, though a data center trade group welcomed efforts to create a more uniform process nationally.

Reply comments are due Dec. 5. DOE asked FERC to issue a final rule by April 30. Below are highlights from a handful of those comments.

Grid operators

Directing regional transmission organizations and independent system operators to develop large-load interconnection queues could spark litigation and uncertainty over jurisdictional issues, according to the PJM Interconnection.

“PJM encourages FERC to seize available opportunities to issue nearer-term regulatory guidance on matters squarely within its wholesale and transmission jurisdiction about: resource adequacy, the provision of ancillary services, mandatory operational regimes, potential wholesale rate classes for different types of load customers, interconnection and transmission planning, cost allocation, and [North American Electric Reliability Corp.] and tariff reliability obligations and requirements,” PJM said.

The Midcontinent Independent System Operator told FERC that adopting standardized large load interconnection procedures could negate existing state-driven interconnection processes and work that has already been undertaken and is ongoing. States have approved or are considering more than 60 large load tariffs, according to the Smart Electric Power Alliance.

FERC should allow MISO and others to continue focusing on efficiently interconnecting large loads under processes that reflect the unique circumstances of their members, states, stakeholders and transmission systems, the grid operator said.

As an alternative to setting standardized rules, FERC could issue a “policy statement” to guide the industry processes for large load interconnections, MISO said.

Investor-owned utilities

The Edison Electric Institute, a trade group for investor-owned utilities, agreed with the DOE that transmission reliability studies must be conducted if existing power plants are going to be used to serve large loads.

“We also underscore that resource adequacy is a growing concern across the country; taking any generation that provides such service off the grid to serve a new large load raises significant reliability and affordability concerns,” EEI said. “The Commission must grapple with this reality and consider additional reforms to ensure that necessary incremental generation resources are available to address any resource adequacy concerns.”

Instead of paying for network upgrade costs, large loads should pay for their use of the transmission system, EEI said, noting that integrating large load customers will require “unprecedented” investment in transmission systems.

“Those investments must be made in a constructive and predictable environment that provides the opportunity to earn a return of and on the entirety of the transmission network, including the transmission upgrades necessary to interconnect new large loads,” EEI said.

FERC should clarify as soon as possible that existing large load processes and agreements will be unaffected by any new rules, EEI said.

Power suppliers

FERC’s rulemaking process should not affect advanced transactions or arrangements between large load customers and power suppliers or delay proceedings like the commission’s investigation into PJM’s rules for co-located loads, according to the Electric Power Supply Association.

Any new load interconnection process should allow for competitive transmission providers to participate in interconnecting large load projects, EPSA said. Also, any new processes shouldn’t affect the existing generation interconnection queue and they should respect competitive wholesale power markets, the trade group for independent power suppliers said.

Considering resource adequacy issues in deciding whether and at what cost to interconnect new large load would discriminate against that load and existing generators, according to EPSA.

“Under fundamental open access principles, there can be no such differentiated treatment between new and existing load or between new and existing generation,” the trade group said.

Data centers

In contrast to lawmakers and regulators, the Data Center Coalition expressed support for a standardized process, with caveats.

Currently, there is a patchwork of rules governing large load interconnections across the United States, creating uncertainty and delaying investments, according to the coalition.

“A more transparent, predictable and uniform approach to large load interconnections, particularly at the transmission level, would provide substantial benefits in terms of coordination, system reliability and economic development,” the DCC said.

Any new rules from FERC would need to have transition provisions that allow existing large load agreements and tariffs to continue under their terms and don’t require new interconnection studies for advanced stage projects, the group said.

Rules should also support stand-alone data centers that procure power from the wholesale market and other sources, according to the DCC.

Ratepayer advocates

Ratepayer advocates slammedDOE’s proposalas an “unprecedented expansion” of FERC’s jurisdiction that lacks key details and relies on inaccurate claims and unsupported statements, the National Association of State Utility Consumer Advocates said.

By allowing generators to directly serve large loads, the proposal ignores state laws that give utilities the exclusive right to serve customers in their service territories, NASUCA said.

“The [proposal] implies that large loads could bypass retail providers in states that do not have retail choice in order to take power directly from a wholesale market,” the group said.

NASUCA decried DOE’s April 30 deadline for a final decision from FERC.

“It is patently unreasonable and would be bad public policy for FERC to use an expedited process to extend its jurisdiction in an unprecedented manner and attempt to develop the implementation regulations necessary to protect traditional retail loads from improper cost shifts,” NASUCA said.

Article top image credit: Mario Tama via Getty Images

Are sodium-ion batteries finally ready to compete with lithium?

Proponents say sodium-ion batteries degrade more slowly, operate more efficiently and have lower fire risk. But high-profile failures cloud the U.S. market.

By: Brian Martucci• Published Oct. 28, 2025

Last month, on the high prairie east of its hometown, Denver-based Peak Energy powered up what it says is the United States’ first grid-scale sodium-ion battery installation and “the first ever fully passive megawatt-hour scale battery storage system” anywhere in the world.

Peak’s 3.5-MWh project marks a big step forward for the electrochemical battery chemistry that many experts believe is the most viable challenger to lithium-ion, which today dominates the energy storage market for discharge durations shorter than four hours.

“What’s nice about our technology is the way it looks and feels to a customer is like a new variant of a [lithium-ion battery] system,” said Landon Mossburg, CEO and cofounder of Peak Energy.

Sodium-ion batteries’ allure is growing amid volatile commodity pricing and an on-again, off-again trade war between the United States and China affecting lithium-ion batteries.

Sodium-ion storage has a simpler supply chain that eschews traditional battery metals, said Evelina Stoikou, an energy storage analyst with BloombergNEF. The U.S. has the world’s largest known reserves of soda ash, a sodium precursor that is more abundant globally than lithium, nickel and cobalt.

“Lithium-ion costs remain highly sensitive to raw material prices, meaning that spikes in lithium, nickel, or cobalt prices could improve sodium-ion’s relative competitiveness,” she said.

But Stoikou cautioned that swingy raw materials pricing can cut in the other direction. At the moment, rapidly-falling LFP costs are driving a boom in global lithium battery deployments.

“Expectations among [sodium-ion battery] manufacturers have cooled as LFP prices continue to trend downward, leading to a reduction in our expectations for sodium-ion to scale,” she said.

Sodium-ion proponents like Peak Energy believe sodium-ion chemistry, though less energy-dense than lithium, has inherent advantages that will allow it to compete on cost before the decade is done. Those include lower fire risk, higher discharge rates, more efficient thermal management and better performance in extreme hot and cold conditions. Mossburg estimates his batteries cost 20% less to operate over 20 years than an equivalent lithium-ion system.

China charges ahead on sodium-ion

As debate rages over sodium-ion batteries’ place in the global energy mix, sodium-ion battery manufacturers and developers are moving forward — particularly in China.

In fact, Peak’s groundbreaking Colorado installation also looks puny next to recent sodium-ion deployments in the world’s second-largest economy. One Chinese state-owned power company is developing a 100 MW/200 MWh installation. Another recently commissioned a 200 MW/400 MWh hybrid sodium/lithium facility that it says reduces system costs by 30% over a sodium-ion-only equivalent. Industry analysts and insiders credit the advancements to the Chinese government’s supply-side subsidies and product standardization.

“Much of the know-how and production for sodium-ion batteries is concentrated in China [and] initial deployment of new-generation sodium-ion products will continue to be in China,” Stoikou said.

China’s sodium-ion push is reminiscent of its decade-long strategy to dominate the market for lithium-ion battery precursors, materials and components. Its head start leads some Western analysts and entrepreneurs to conclude that China will also dominate the sodium-ion battery market, at least for grid-scale energy storage applications.

Others, including Peak Energy, are making a different bet. As production scales up in China and eventually the United States, they expect sodium-based battery producers to carve out a sizable share of the rapidly-growing stationary storage market worldwide — not only in China. BloombergNEF expects global stationary storage capacity to grow 12-fold over the next 10 years.

High-profile failures sow doubts in U.S. market

Clouding that optimistic vision is the recent failure of Natron Energy. The once high-flying sodium-ion battery startup folded in September, barely a year after announcing plans to build a $1.4 billion, 14-GW manufacturing facility in North Carolina. It was the second U.S. sodium-ion company to go bankrupt in 2025. Stanford University spinout Bedrock Materials closed in April, citing technical and market challenges.

Yet even sodium-ion skeptics like Stanford University scientist Adrian Yao, lead author on a widely-cited January paper questioning the technology’s near-term commercial potential, warn against reading too much into Natron’s failure. Yao told IEEE Spectrumearlier this month that Natron may have been too early to its chosen niche: high-powered, short-duration batteries for data centers and large industrial facilities.

“Hyperscalers right now, their primary concern is just getting connected and building data centers,” he said. “I think timing on that cycle may be early.”

Where ‘sodium excels’

According to Unigrid cofounder and CEO Darren Tan, less energy-dense but higher-power sodium battery modules are indeed better suited to shorter-duration applications. Those include backup and demand response for commercial and industrial users, a niche Natron aimed to fill with its first products.

“Fifteen to 60 minutes is the real market now — that’s where lithium struggles and sodium excels,” Tan said in an interview.

Isshu Kikuma, another BloombergNEF energy storage analyst, said in an email that steadily falling prices mean lithium-ion batteries are now cost-competitive at durations of six to eight hours in some geographies. For years, energy storage experts have expected flow batteries — whose active ingredients are typically petroleum-based or metals heavier than lithium and sodium — and more novel technologies to dominate durations longer than four or five hours.

That’s one reason Tan believes sodium-ion is not in a position to challenge lithium-ion in grid-scale stationary storage. He also blames China’s head start on commercialization and its ruthlessly competitive clean tech culture, which drives prices far below levels Western manufacturers can match.

“If sodium is ever cheaper than lithium, it will be the Chinese who win, same as today,” he said.

At least in the near term, Unigrid is focusing on opportunities outside the world of stationary storage. For example, Tan said Unigrid’s power cell batteries are ideal drop-in replacements for traditional lead-acid car starters — a $15 billion opportunity, he said.

“That’s an existing market, not a projected one,” Tan said, alluding to the fact that sodium batteries’ grid-scale storage potential remains largely untested.

In the longer run, Tan said sodium-ion chemistry could eat into lithium’s dominance in behind-the-meter storage at shorter durations.

Because they’re less energy-dense, sodium-ion batteries have a lower risk of thermal runaway, the electrochemical process that can lead to battery fires like the January conflagration that consumed a 300-MW battery array on the central California coast. With encouragement from Environmental Protection Agency Administrator Lee Zeldin, communities around the country have tightened restrictions on lithium-based energy storage or frozen their development entirely since the fire at the Moss Landing energy facility.

“Commercial businesses, data centers, residences in urban environments — these are areas where safety is important,” Tan said.

Peak Energy says its time has come

Peak Energy’s Mossburg has a different view. He believes a particular variety of sodium-ion battery can compete at utility scales and that price parity with lithium will come sooner than the skeptics expect.

The active cathode ingredient in the batteries at Peak Energy’s Colorado facility is sodium pyrophosphate, or NFPP. In an interview, Mossburg said Chinese investment flows this year indicate NFPP chemistry is edging out other sodium-ion varieties in the world’s biggest battery market, likely lifting U.S.-based NFPP developers.

“Most of the investment is happening in NFPP, which wasn’t clear when we made the call,” Mossburg said.

In a July press release, Peak Energy touted its passively-cooled batteries’ advantages over lithium-iron-phosphate chemistry, or LFP. LFP is the lithium-ion variant that accounts for most stationary storage facilities being built today.

One big advantage is a 90% reduction in auxiliary power use — a direct benefit of passive cooling. Grid-scale LFP batteries draw significant amounts of power to run the active cooling systems needed to prevent thermal runaway, reducing their cost-effectiveness. Peak says the difference can save operators $1 million or more per year, per GW.

Peak also says its batteries are more durable, degrading 33% more slowly over a projected 20-year lifespan. All told, lifetime costs come in 20% lower than comparable LFP systems, Peak says.

In hot climates with more intense cooling loads for LFP batteries, Mossburg said NFPP operators could save $5/kWh to $10/kWh. Sodium-ion batteries also hold their charge better in very cold conditions, making them more efficient year-round in northern climates, Mossburg said.

Mossburg said his batteries’ performance advantages are winning over risk-averse customers seeking competitive returns on energy equipment. He said the company plans to announce new customers soon.

“The way we’re winning deals now is by going head-to-head against incumbents [like] CATL and Tesla,” he said, naming two major lithium-ion players. “We win because our technoeconomics are better.”