This article is part of Utility Dive’s 2023 U.S. Power Sector Outlook series. A roundup of all the articles is available here.

Work to build tomorrow's distribution system will accelerate in 2023 and bring three new insights about distributed energy resources, or DER, despite challenges, analysts say.

Uncertainties remain about customer DER adoption and the need for distribution system control technologies, power system stakeholders agreed. But the numbers leave no doubt about fast-rising penetrations of electric vehicles, charging infrastructure and customer-owned solar, batteries and heat pumps, along with smart thermostats, appliances and other devices.

Electric utilities expect customers to “deploy and explore DER for electrification in 2023 across many different technologies and end uses,” said Patricia Taylor, director of Policy Research and Analysis at the American Public Power Association. And the importance of DER “load flexibility” value is growing “as intermittent renewables replace retiring traditional baseload resources,” she added.

Even when some state regulators reduced compensation for DER like residential solar in 2022, they added opportunities for DER like solar-plus-storage in 2023 that offer reliability and resilience, stakeholders noted.

“Reliability is a concern virtually everywhere, making once risk-averse regulators, utilities and other stakeholders more open-minded” about DER, said Generac VP, Markets and Programs, Josh Keeling, a former Portland General Electric executive. That urgency “will lead to important decisions in 2023 to advance DER,” he added.

To meet federal and state electrification and decarbonization policies, 2023 will see major advances for DER aggregations in wholesale markets and at the distribution system level, utility representatives, DER advocates and policy analysts agreed. And 2023 may also see new community and consumer stakeholders take a more central role in driving growth, some experts said.

The data says growth

Despite supply chain constraints, residential solar’s “historic” Q3 2022 1.57 GWdc growth in the U.S. was 43% higher than Q3 2021, according to the Q4 2022 Solar Market Insight report from Wood Mackenzie and the Solar Energy Industries Association. And 2022’s estimated 5.8 GWdc installed capacity is expected to reach an estimated 6.2 GWdc in 2023 and 7.5 GWdc in 2027, the report projected.

Uncertainties about Inflation Reduction Act tax credits and adders could limit growth, Wood Mackenzie cautioned. But “the fundamentals for residential solar are strong” because “customers crave energy independence and savings” to offset rising retail electricity rates, it added.

Residential energy storage’s 161 MW/400 MWh of new capacity in the U.S. in Q3 2022 was also a record, significantly exceeding Q3 2021’s 111 MW/258 MWh, The Q4 2022 Energy Storage Monitor from Wood Mackenzie and the American Clean Power Association reported. Annual residential energy storage capacity, estimated at under 1.5 GW for 2022, is likely to reach over 2.2 GW in 2026, it added.

Sales of U.S. electric heat pumps will also grow steadily, according to American Heating and Refrigeration Institute data. The over 13 million electric heat pumps in the U.S. in 2021, which includes geothermal heat pumps, were projected to reach almost 14 million in 2022 and 14.3 million in 2023, according to the Energy Information Administration March 3, 2022, Annual Energy Outlook.

An estimated 15% increase in North America’s energy efficiency investments from 2015 to 2022 reduced U.S. energy consumption 30% in 2021 and should support continued reductions, according to a Dec. 20 industry report.

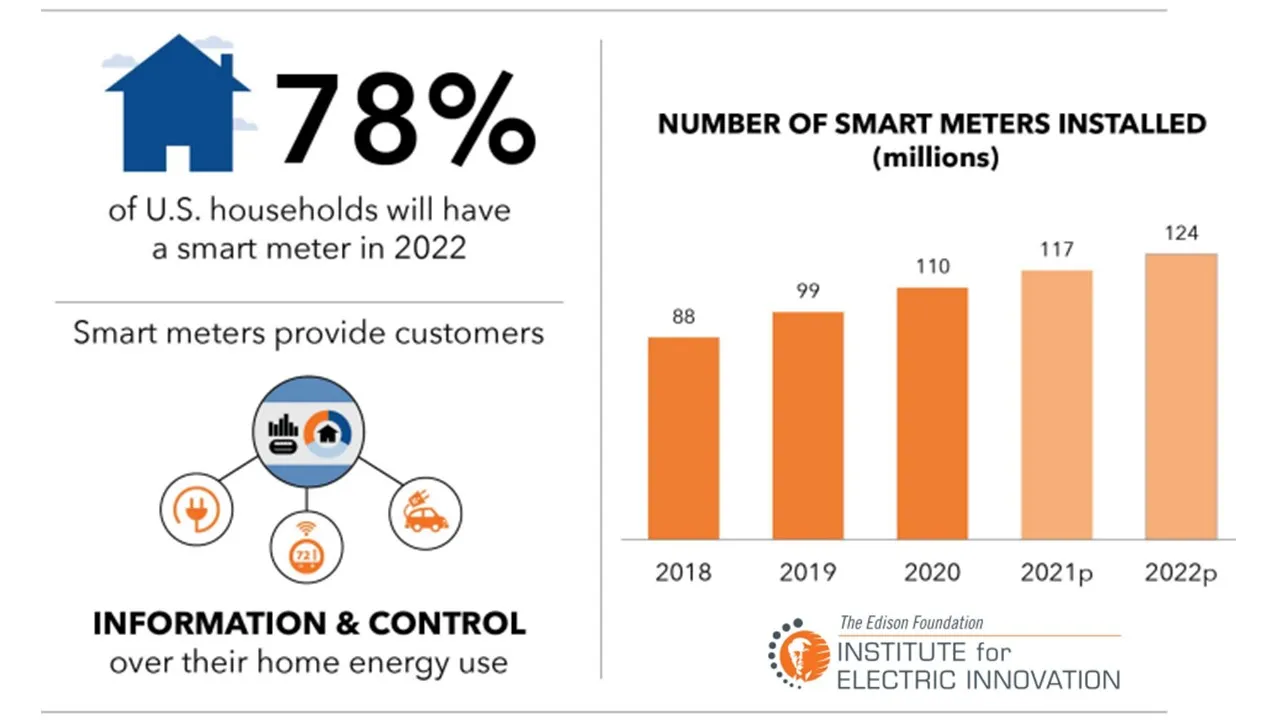

April 2022 data from the Edison Foundation’s Institute for Electric Innovation projected there would be over 124 million smart meters installed in 78% of U.S. households by the end of 2022. Sustained market growth is projected to reach nearly $3.3 billion in revenue in 2028, a February 2022 Fortune Business Insights report forecast.

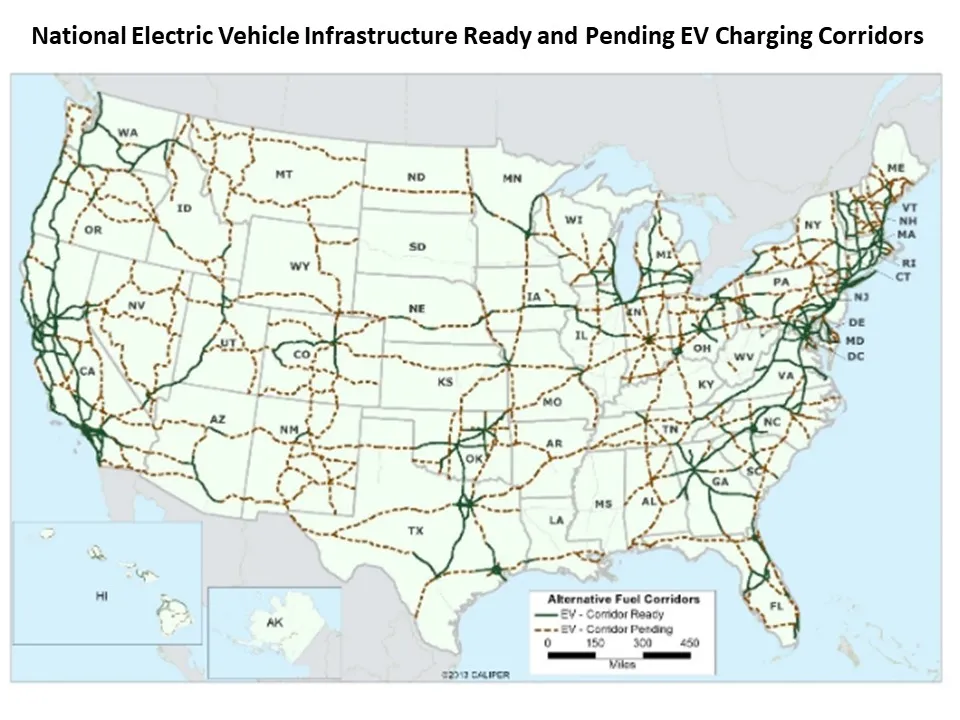

More than 2.7 million electric vehicles had been sold in the U.S. through June 2022, the Natural Resources Defense Council reported in October. And EVs’ 1% share of the U.S. light-duty vehicle market is growing, with EV’s H1 2022 sales growing 41% from H1 2021 while total H1 light-duty vehicle sales fell 22%, a Sept. 13, 2022, Alliance for Automotive Innovation report said.

The U.S. EV market’s $28.24 billion value in 2021 will reach $137.43 billion in 2028, another February 2022 Fortune Business Insights report forecast. But new public charger installations are not keeping up with the growth of EVs, sources agreed.

To rectify the estimated 33 EVs per outlet ratio found in mid-2022, regulators are streamlining charger deployment approvals for utilities and for the federally funded National Electric Vehicle Infrastructure Program, the North Carolina Clean Energy Technology Center, or NCCETC, November 2022 EV policy update reported.

Across all DER technologies, new policies to accelerate deployments are expected in 2023, added NCCETC Associate Director of Policy and Markets Autumn Proudlove and others monitoring state regulatory activity.

Regulatory review

Throughout 2022, policymakers considered over 600 transportation electrification-related policy actions like financial incentives, market development and regulation, NCCETC reported.

There were also nearly 600 policy initiatives impacting distribution system modernization across 2022, NCCETC’s October 2022 Q3 grid modernization policy update showed. Actions included utility business model reforms, smart grid and smart meter deployment, distribution system planning, energy storage and time-varying rates, NCCETC reported.

And in Q3 2022 alone, 40 states and D.C. were working on policy actions about net energy metering, or NEM, or other DER compensation, rate and billing structures, the NCCETC October solar policy update added.

Policies supporting access to DER for disadvantaged communities also grew across all technology types, NCCETC’s Proudlove said.

Another “general trend” that could see more regulatory approvals in 2023 is time-of-use, or TOU, rates with added low-priced off-peak periods, Proudlove said. Such TOU rates, and innovative demand charge structures that prevent bill spikes at public or fast chargers, can add to the savings and appeal of driving electric, she added.

Broader reforms like Maine’s beneficial electrification rates may become more common in 2023, Proudlove said. Rather than simple TOU rate changes, Maine carefully revised demand charges for EV drivers and battery storage owners to improve the economics and reduced heat pump rates to encourage adoption, she said.

Three grid modernization trends — performance-based regulation, rate designs for energy storage, and all-source competitive procurements by utilities — could be advanced by a wide range of new regulatory initiatives in 2023, including approval of performance incentives in Illinois and requirements for competitive bidding in New Mexico, NCCETC said.

Finally, 2023 will advance California’s work to bring distributed resources into the marketplace in its CalFUSE and High DER proceedings, NCCETC and stakeholders agreed. It will have minimal impact on near-term market activity, but the regulatory dialogue can advance understanding of how DER’s demand flexibility, supported by real-time pricing and market architectures, can participate and benefit system reliability and customers, they said.

California’s Dec. 15 decision on NEM reduced customers’ compensation for exported generation and could contract the state’s nation-leading solar market in 2023, Wood Mackenzie reported.

But the decision’s state and national influence in 2023 will not necessarily be entirely negative because it also expanded DER’s reliability value when paired with distributed storage, some stakeholders said.

North and South Carolina may have successor tariffs to retail rate NEM in 2023 that increase compensation for DER that supports system needs, Proudlove said. Other states are adding compensation for DER like battery storage in demand response programs that provide system resilience and reduce costs, she added.

Finally, Texas regulators in January approved the Aggregate Distributed Energy Resource Pilot Project to evaluate DER aggregations in the state’s wholesale markets, said Proudlove. Other state planning is similarly “getting out ahead” of the Federal Energy Regulatory Commission Order 2222 effort to use DER in wholesale markets, Proudlove said.

The wholesale market advance

Regional transmission organizations and independent system operators were ordered in September 2020 “to remove barriers to the participation of DER in the capacity, energy and ancillary service markets,” by FERC Order 2222.

When and if the order will enable DER aggregations to compete with traditional energy, capacity and ancillary services market resources are likely to become clearer in 2023, FERC watchers agreed.

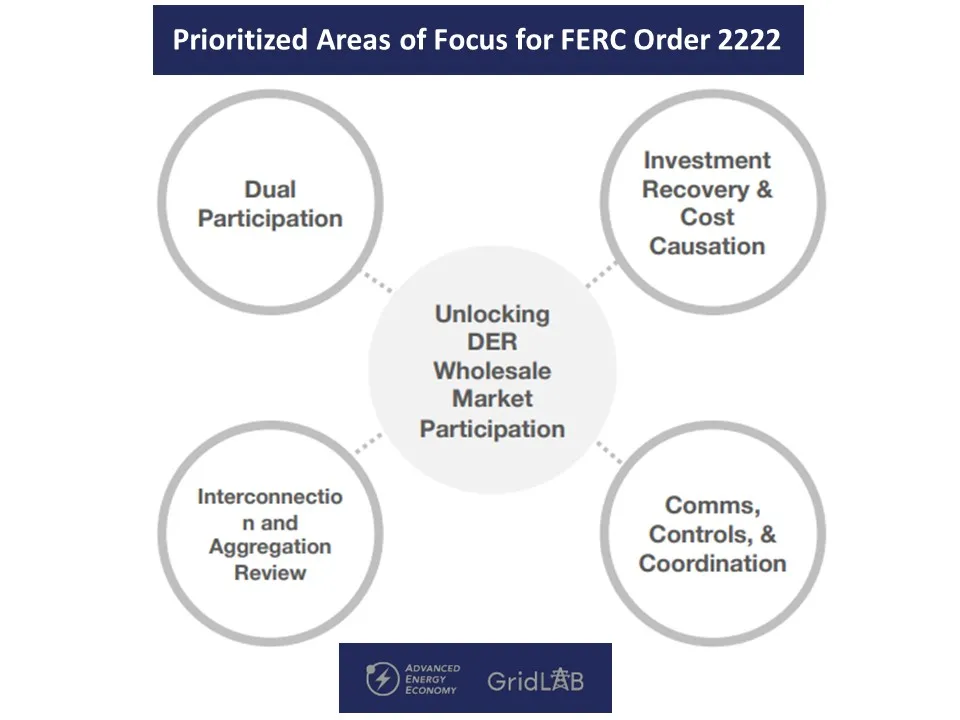

Rules for wholesale market integration should evolve with DER technologies’ scale and types of services, a January 2022 report by GridLab and Advanced Energy Economy, or AEE, analysts said. Key issues will be interconnection procedures, cost and benefit assessments, and management and coordination of dual participation in wholesale and retail markets, the report said.

Compliance filings from system operators on implementing Order 2222 were due July 19, 2021, but only the California ISO and the New York ISO submitted them, said AEE Managing Director Caitlin Marquis. FERC’s ruling on extension requests from PJM, ISO-New England, the Midcontinent ISO and Southwest Power Pool may come in 2023, she added.

The recently approved NYISO market design submitted in 2019 will likely allow DER and DER aggregations to participate in NYISO energy, capacity and ancillary services markets in 2023, Foley Hoag Counsel Devlyn Tedesco said.

“Multi-state organizations have more challenges designing compliance plans because each state has its own regulation,” Marquis acknowledged. Bidding across broad geographic regions and dual participation in both wholesale markets and retail utility programs are particularly complicated, making implementation of Order 2222 by 2026 a “reasonable” expectation, she said.

Order 2222 may be the path to DER growth through federal regulation, but more significant DER integration may be possible through state regulatory action at the distribution system level, some experts said.

Sunrun’s 2022 participation in the ISO-NE capacity market was possible because of “pre-Order 2222 bidding pathways,” said Sunrun Policy Director Chris Rauscher. But Order 2222 “will not open up new opportunities for Sunrun because minimum asset sizes and market participation requirements do not suit residential DER” operational patterns, he said.

Customer demand for DER cost savings, reliability and resilience is, however, “a clear signal to regulators and policymakers to find ways to integrate them,” Marquis, Tedesco and Rauscher agreed.

The distribution system advance

DER aggregated in utility-led “bring your own device,” or BYOD, programs, and virtual power plants, or VPPs, “have become proven grid resources,” said Sunrun’s Rauscher. “Utilities with reliability challenges are coming to DER providers for solutions,” he added.

System integration of the reliability and resilience potentials of BYOD programs and VPPs may be advanced in 2023 more by state regulation than by FERC Order 2222, DER providers and utility representatives said.

A Sunrun VPP announced in November for 2023 operation by PREPA, Puerto Rico's dominant power provider, will function with nearly the reliability of “a base load resource, by discharging solar-charged batteries an estimated 260 days a year,” said Rauscher. And because VPPs are on customers’ roofs and in their garages, they can be built “without interconnection queue, siting and permitting, or political opposition issues,” he added.

In response to an anticipated need of more than 3 GW of DER through 2045, Puget Sound Energy, or PSE, is developing a “platform” of “sophisticated software applications” to manage an “evolving” VPP, said PSE Manager of Strategic Initiatives, Elaine Markham.

PSE’s VPP platform will begin with integrating BYOD-like demand response programs and later expand to battery energy storage and multi-DER VPP-like programs, Markham said. Additional aggregators and new technologies will be integrated as customers acquire DER and the technologies evolve, she added.

The amount of system technology needed “depends on the utility and its community’s goals,” APPA’s Taylor said. At public power utilities, “more DER pilots are being done, especially in transportation electrification, and important lessons learned are being shared,” she added.

Dispatch of Sunrun-aggregated East Bay Community Energy's, or EBCE’s, already installed 1,500 solar-plus-storage systems, does not require expensive system technology, said EBCE CEO Nick Chaset, a former California Public Utilities Commission staffer. In 2023, EBCE will expand its VPP and a managed EV charging programs with “a customer-first approach,” he added.

Arizona Public Service, or APS, plans to expand both a BYOD program for smart thermostats, and a multiple DER aggregator residential battery VPP in 2023, APS Spokesperson Yessica Del Rincon said. And Sacramento Municipal Utility District, or SMUD, has similar VPP plans and will expand an EV-managed charging pilot with GM, Ford and Volkswagen this year, SMUD Spokesperson Gamaliel Ortiz said.

Many 2023 DER aggregation efforts also include an equity goal.

Avista Utilities will initiate a DOE-supported Connected Communities project in 2023 to “equitably” integrate utility-dispatched VPPs from grid-connected efficient buildings, Avista spokesperson Casey Fielder said. And a public power utilities Energy Transition Community working group is working to advance both DER integration and equity, APPA’s Taylor said.

That focus on equity is leading to the emergence of new voices in power system regulation and planning.

The new voices advance

Greater engagement by local leaders in regulatory and legislative decisions on DER will be more common in 2023, analysts said.

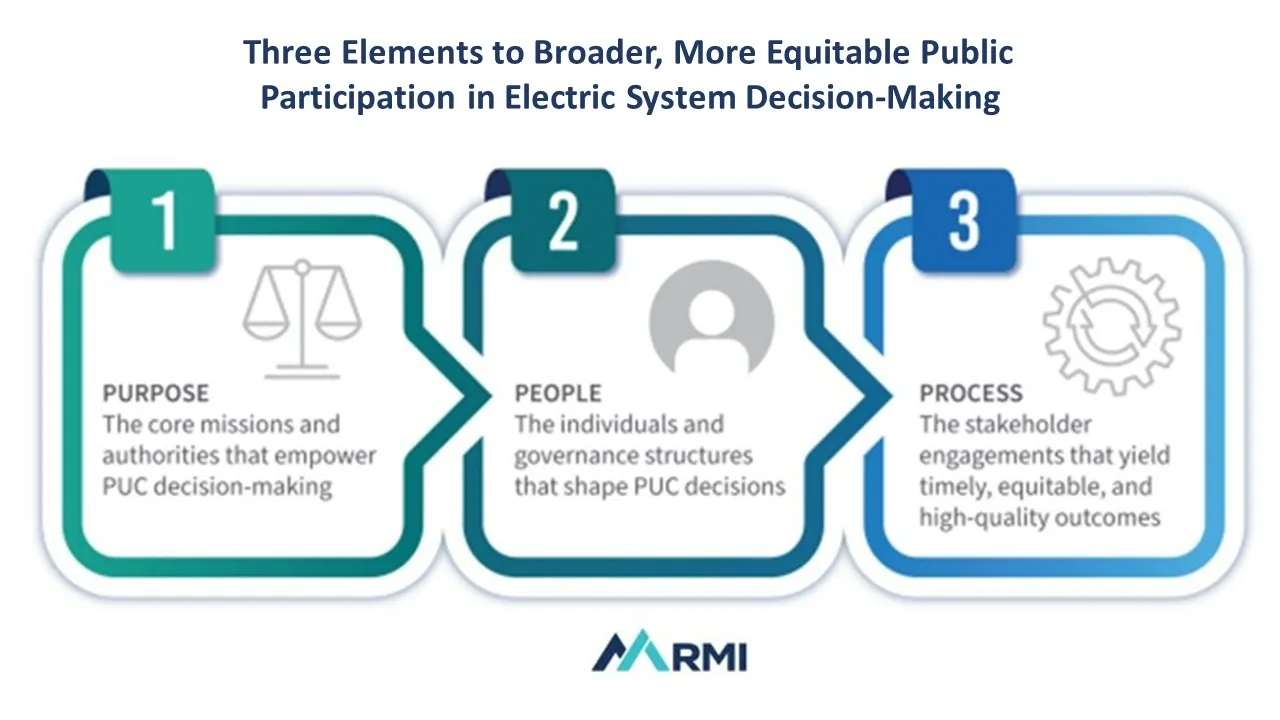

“The utilities, the distribution system, and its rules should serve the needs of the community, not the other way around,” California Alliance for Community Energy Coordinator Al Weinrub told state agency and utility representatives in a Gridworks-led California High DER Future workshop last June.

Local government, community and tribal leaders “detailed engagement on energy and climate issues could lead a California energy policy evolution,” Gridworks Executive Director Matthew Tisdale said. “Thinking globally and acting locally is new to some policymakers, but hearing local leaders can allow them to see challenges from new angles,” he added.

A “national initiative” with input from the full range of stakeholders is needed to build a framework for DER integration, according to a recent DER sector analysis. “DER technologies are reaching maturity just as the need for reliability becomes urgent, but balancing local and central control and interests remains an unanswered question,” added Generac’s Keeling, who co-authored the analysis.

“Utilities favor central control, but DER technologies are coming so quickly that some aggregation seems necessary” to protect distribution system operations, Keeling added. Municipal, community and local leaders can be critical in resolving the unanswered question because they have a different perspective than regulators or utility leaders, and “that can lead to new approaches,” he said.