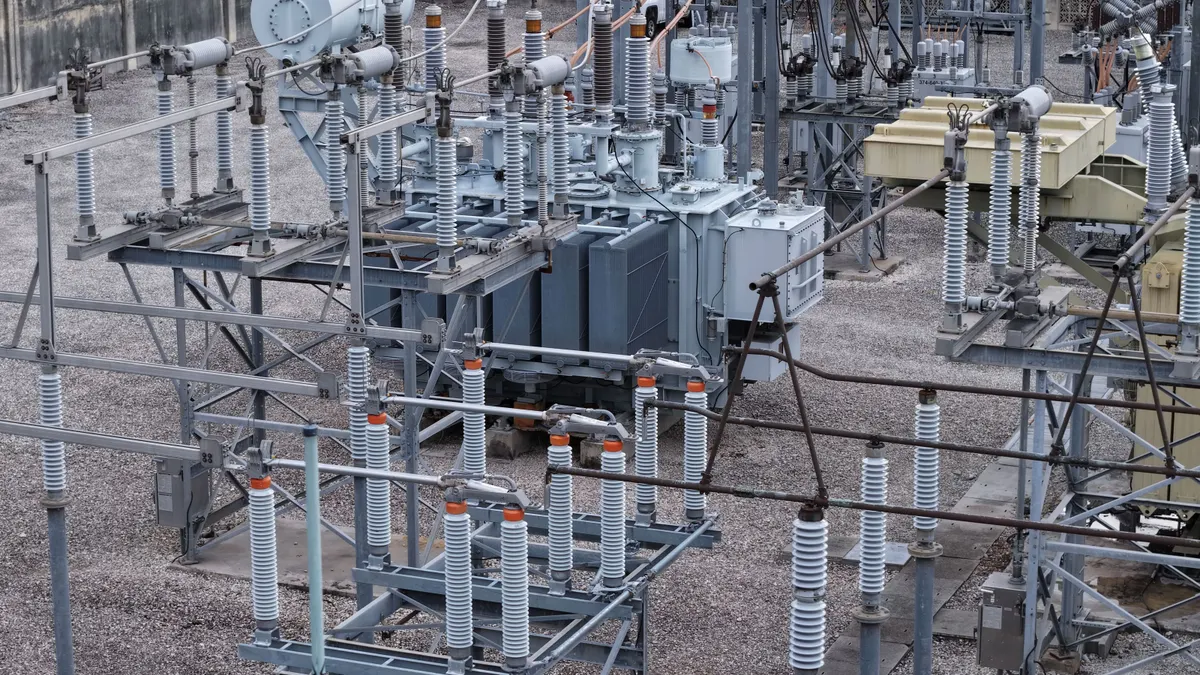

In the past two years, at least six advanced reactor designs have begun operations or made significant progress at the Nuclear Regulatory Commission, the United States’ primary nuclear regulator.

Advanced reactors promise greater safety, quicker deployment and less cost than traditional nuclear generation. But skeptics warn that the technology remains largely unproven in the Western world and that early deployments may cost significantly more than advertised.

More recently, the NRC has accelerated reactor construction permit reviews, allowed approved reactor designs to remain valid longer and eased restrictions on certain factory-built reactors. More NRC reforms are on the way.

Advanced nuclear energy is on the upswing thanks also to supportive state policy, expected load growth, technology companies’ interest in “clean firm” power and federal tax incentives that largely survived GOP budget negotiations, ClearView Energy Partners said in a July 3 research note.

These tailwinds have many utility leaders planning for a future generating mix that includes new nuclear. For those that aren’t, now is the time to get up to speed.

Defining “advanced nuclear”

Despite being “as different from one another as gouda and gorgonzola,” all advanced reactors have simpler and less failure-prone safety systems than those securing the vast majority of currently operating reactors, according to the Nuclear Innovation Alliance, a Washington, D.C.-based trade group that put out a comprehensive primer on advanced nuclear technologies last year. Most of these systems are at least partially passive, meaning they don’t require human intervention to activate.

The most expansive definition of advanced nuclear encompasses large light-water reactors like the two 1,117-MW AP1000s now in operation at Georgia Power’s Vogtle power plant — whose final price tag of about $32 billion more than doubled the $14 billion preconstruction estimate — as well as tiny microreactors like the 1-MW molten salt design under construction at Abilene Christian University. In between are modular reactors — known as micro- or small modular reactors, depending on their output — that can be partly or even largely built in a factory and then transported to the generating site.

Experts say smaller reactor designs may prove faster and cheaper to deploy than larger ones, advanced or otherwise. The U.S. Department of Energy in September estimated the total project cost for a first-of-its-kind small modular reactor at $4 billion, or one-third the expense of a larger reactor. A British study released in 2018 found that full modularization could reduce capital costs by more than 40%, excluding interest charges.

But large advanced reactors may always be more cost-effective for bulk electricity generation, DOE says. The department pegs costs for a first-of-a-kind large light-water reactor at about $8,500/kW, compared with about $13,000/kW for an early SMR, and flags large reactor build costs as low as $2,300/kW in South Korea after decades of process improvement there.

What’s next for advanced nuclear

Cost concerns led to the cancellation in late 2023 of NuScale’s 462-MW Carbon Free Power Project, which until this May was the United States’ only commercial SMR project for a utility offtaker.

The project’s cancellation was a big setback for the nearly 20-year-old Oregon company and advanced nuclear more broadly.

Though NuScale remains a subcontractor on a power plant project in Romania and says it’s close to signing offtake agreements with non-utility customers in the United States.

It was also a teaching moment for the industry, said Judi Greenwald, executive director of the Nuclear Innovation Alliance.

“[NuScale] put all their eggs in one basket [and] that one entity wasn’t enough of a business case,” she said, referring to the coalition of Western municipal utilities that would have purchased power from the project.

Likewise, NuScale’s often halting regulatory engagement with the NRC — the company got approval for a 50-MW module in 2020, then returned for the 77-MW module the NRC greenlighted in May — provided a model for future nuclear technology companies to engage and made the agency itself more efficient, Greenwald said.

“NuScale paved the way for a lot of other people,” she said. “They spent a lot of time with NRC, some of it not as fruitful as we would have liked, and a lot of others are going to get the benefit.”

Those lessons and landmark pro-nuclear laws passed in 2019 and 2024 have pushed the NRC to speed up its reactor design, construction permit and operating license application reviews; develop a lighter-touch framework for microreactor licensing; and establish a new “risk-informed, technology-inclusive” licensing pathway for advanced reactors.

The upshot could be faster, more efficient approvals for all sorts of advanced nuclear technologies, particularly microreactors, said James Richards, manager of NIA’s economics and project development program.

“Microreactor developers are very much anticipating going faster,” he said. “The regulatory environment has changed and is changing.”

The nuclear technology companies that came up behind NuScale have diverse business and development models, Greenwald and Richards said.

Kairos Power, Greenwald said, follows an “innovation model” that relies on low-power test reactors to perfect their technology and minimize future licensing challenges on the way to commercialization.

GE Hitachi is following a more direct route to commercialization by partnering with big, innovative utilities willing to take risks on a first-of-its-kind project.

Holtec International plans to develop SMRs on existing nuclear power plant sites with spare interconnection capacity, beginning with the soon-to-be-restarted, 800-MW Palisades generating station in southwestern Michigan.

X-energy’s first commercial project will supply process heat and electricity at a Dow petrochemical complex in Texas, replacing the facility’s aging, fossil-fired cogeneration plant. Along with TerraPower, X-energy has significant support from the DOE Office of Clean Energy’s Advanced Reactor Demonstration Program.

And Last Energy is pursuing front-of-the-meter and behind-the-meter arrangements with data centers and other large power consumers interested in its 20-MWe modules.

“If you can cut through the noise, there is real stuff happening in the industry right now — shovels in the ground,” Richards said. “We haven’t seen this since the 1980s, and we’re seeing it with new and different designs”

Advanced nuclear reactor types

All commercial reactors operating in the U.S. today use steam or superhot pressurized water to generate electricity and cool cores powered by low-enriched uranium.

Some advanced reactor designs envision doing the same, but not all. A fair number use liquid metal, molten salt or high-temperature gas for cooling and heat transfer. Many of these more novel designs — including those from Kairos Power, TerraPower and X-energy — will use more potent high-assay, low-enriched uranium, which allows for more efficient reactions in compact reactors with longer refueling cycles.

HALEU-powered non-water reactors can reach higher outlet temperatures than water-cooled reactors, making them suitable not just for electricity generation but for industrial heat production as well, according to an Information Technology & Innovation Foundation paper published earlier this year.

Five varieties of advanced reactor stand out right now. For each of the five, read below about potential applications the ITIF paper identifies and a project or developer reasonably far along in the demonstration process.

Pressurized water reactor (PWR)

Potential applications: Power generation, lower-grade industrial heat (desalination, pulp and paper, some petrochemical applications)

Example project: AP-1000s at Plant Vogtle Units 3 and 4, Georgia Power — Waynesboro, Georgia

Pressurized water reactors have powered conventional nuclear plants for decades. The reactor core heats a pressurized water loop that generates steam in a secondary, lower-pressure loop that powers a turbine generator.

PWR technology factors into several advanced nuclear designs, including NuScale’s US460, Holtec International’s SMR-300, Last Energy’s PWR-20 and Westinghouse’s AP1000 and AP300 SMR.

Boiling water reactor (BWR)

Potential applications: Power generation, lower-grade industrial heat

Example project: BWRX-300 at Clinch River Nuclear Site, Tennessee Valley Authority — Clinch River, Tennessee

The boiling water reactor is the other mainstay of the U.S. conventional nuclear fleet. The reactor core heats and partially boils pure water, which — after some twists and turns — produces pure steam to power the main generator.

The technology isn’t as popular with SMR developers, but there is one standout: GE Hitachi’s BWRX-300, which has made significant progress toward commercialization. One is already under construction at Ontario Power Generation’s Darlington nuclear plant and could come online there by 2029.

Stateside, Tennessee Valley Authority in May became the first U.S. utility to submit an SMR construction permit for a planned BWRX-300 plant that could power up in the early 2030s.

Molten salt reactor (MSR)

Potential applications: Power generation, high-quality industrial heat (hydrogen production, most petrochemical processes, direct steelmaking)

Example project: Hermes 1 and 2, Kairos Power — Oak Ridge, Tennessee

Molten salt reactors use molten salt as a coolant only or as a dual fuel and coolant, according to the International Atomic Energy Agency. In either case, the salt can absorb far more heat than water, allowing the reactors to operate at temperatures high enough to power hard to abate industrial processes like production of plastic precursors.

Some advanced nuclear plant designs, including the next on our list, also use molten salt as an energy storage medium that operates separately from the reactor and generator.

Some nuclear experts see molten salt reactors as an “over the horizon” technology that will mature after BWRs, PWRs and liquid metal reactors, but Kairos Power appears to be making progress toward commercialization. It’s building the first of two test reactors in Tennessee, targeting commissioning in 2027, and has agreed to supply 500 MW of power to Google by the mid-2030s.

Liquid metal reactor (LMR)

Potential applications: Power generation, medium-grade industrial heat (tar sands and shale oil production, petroleum refining)

Example project: Natrium at Kemmerer Power Station Unit 1, TerraPower — Kemmerer, Wyoming

Liquid metal reactors use molten metal, often pure sodium, to cool the core and transfer heat to an electric generator, energy storage medium and/or facilities running medium-temperature industrial or resource extraction processes.

Neutrons move much faster through metal-cooled cores than through water-cooled cores, enabling fast reactor designs that can recycle nuclear fuel and potentially reduce nuclear waste.

Oklo and TerraPower are both working to commercialize sodium-cooled fast reactors. TerraPower broke ground last year at the Wyoming site of its 345-MW Natrium commercial demonstration reactor, which is in line to get its construction permit later this year and could power up by 2030. Thanks to a molten salt energy storage reservoir, that facility will have load-following capabilities to complement the wind-heavy Wyoming grid.

High-temperature gas reactor (HTGR)

Potential applications: Power generation, high-quality industrial heat

Example project: Xe100s at Long Mott Generating Station, Dow & X-energy — Seadrift, Texas

High-temperature gas reactors use helium or another stable gas to cool their cores and transfer heat for electricity production or direct industrial use. They achieve very high outlet temperatures with great efficiency, making them ideal for heavy industries like petrochemicals and steelmaking.

The best-known U.S. HGTR is X-energy’s Xe-100, which is the subject of an active construction permit application and could come online early next decade at Dow’s Seadrift facility.

Like some MSRs and LMRs, HGTRs run on TRISO, a heat-resistant, ceramic-coated HALEU fuel that experts say is more durable than conventional fuel rods. U.S. supplies of HALEU-based fuels remain scarce, though DOE recently made some available to early-mover nuclear companies and domestic enricher Centrus plans to ramp up production later this decade.

Clarification: We have updated this story to clarify the source of potential applications associated with each type of nuclear reactor.