A new market for Inflation Reduction Act clean energy tax credits will bring significant new capital to wind, solar, battery, clean hydrogen and carbon capture projects, financial analysts say.

The IRA transferability provision allowing the buying and selling of federal production and investment tax credits could more than triple the $20 billion annual tax equity market that today finances clean energy in the U.S., the analysts say. Clean energy developers can earn revenues by selling tax credits, buyers can reduce their tax burdens while financing new projects, and utilities could increase ownership of low cost clean energy to reduce customer rates.

Currently, a limited number of very large investors are obtaining tax credits through complex partnership agreements with project developers. The new IRA provision allows much more streamlined sales of tax credits by clean energy developers and a much larger pool of buyers is expected to bring capital to the sector.

Selling tax credits “helps offset costs of the clean energy transition for our customers” and the impact could be “profound,” Duke Energy Vice President for Tax Cooper Monroe said. Duke intends to use transferability and “is considering an auction-style process,” Monroe added. Auctions are typically used to make financial transactions more efficient and transparent.

The Treasury Department’s June 14 guidance on tax credit transfers, or sales, was “comprehensive” and offered “a very clear description of the transaction process,” analysts and attorneys say.

“Tax credit sales are ramping up more quickly than expected,” affirming forecasts of potential $60 billion annual sales in the near term, said Keith Martin, partner and co-head of projects, U.S., for Norton Rose Fulbright, which just facilitated a tax credit sale involving Bank of America Securities. And the new transactions “are likely to increase in 2023 as more investors face year-end tax liabilities,” he noted in June.

The new financing tool may create competition for tax credits from tax burdened investors, financial analysts agree. But the new transactions must still prove to be cost effective and secure for new investors, resolve complications unique to utilities, and the new opportunities for taxpayers must avoid the political backlash of previous tax reallocations, some analysts caution.

Following the money

The promise of tax credit transferability is enormous, analysts and attorneys agree.

“Over $50 billion in just wind and solar tax credits could be transferred in 2024,” Andy Moon, co-founder and CEO of transfer broker Reunion Infrastructure recently told financial analysts Pivotal180. “With new IRA support for hydrogen, carbon capture, and other clean energy technologies, there could be $80 billion per year in tax credits looking to be monetized,” he said.

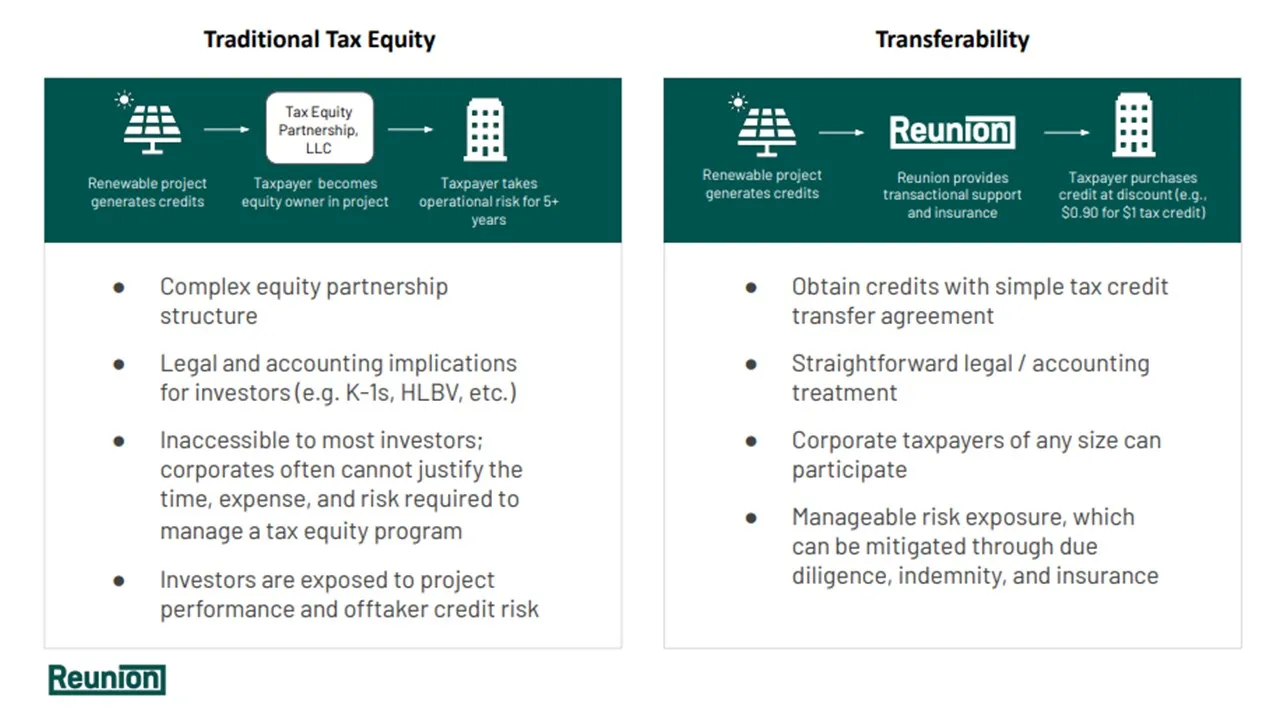

Tax equity partnerships with large investors like Bank of America or J.P. Morgan have been “a great tool,” allowing renewable energy developers to “assign tax credit rights in return for upfront cash equity investments,” added Reunion co-founder and President Billy Lee.

But the legally complex, costly partnership agreements require significant legal and other due diligence work which can cost “up to 15% of the value of the original tax credit,” according to a Center for American Progress summary of transferability.

The “unintended consequence” has been financing going to “the biggest and lowest risk projects,” and has limited tax credit monetization to “around $20 billion per year,” Lee said.

Less costly and complex tax credit transfers are likely to attract more and different types of investors, Lee and Moon said of strategies they are developing to simplify and standardize the new transactions. They will also finance smaller projects and more innovative technologies overlooked by risk averse tax equity investors, they agreed.

Tax credits are currently selling for $0.85 per dollar to $0.95 per dollar, with prices nearer $0.95 for 2023 credits “because sellers know those buyers are eager,” said Becca Glazer, senior director of growth initiatives, for renewables investor AES Clean Energy. Prices for 2024 are “about $0.90,” and even lower for credits in 2025 and later, she added.

“The highest prices of $0.95 are going to utility-scale solar and wind tax credits,” where developers choose transferability instead tax equity, said Norton Rose’s Martin. Unproven technologies’ tax credits are selling at lower prices, he added.

Both availability of tax credits from developers and demand for them from corporate interests are growing, said Generate Capital Principal of Structured Finance, Jessie Robbins. But it is too early to say how it will impact tax credit pricing, or how institutional tax equity investors will react, she added.

The traditional tax equity market “does not yet feel threatened,” and it will take time for transfer transactions to develop streamlined “standardized structures,” Glazer agreed. But “by next year, in a more defined transferability market, tax equity investors are likely to feel more competition,” she said.

“Transferability will not be perfect, but it will be better” than tax equity partnership transactions. “It won’t be simple, but it will be simpler. It won’t be cheap, but it will be cheaper. It won’t be fast, but it will be faster,” responded Segue Sustainable Infrastructure Managing Partner Dave Riester, in comparing tax credit sales to tax equity agreements. “There will be due diligence to perform, but a lot less.” These factors will improve the economics of renewables deployment, he said.

Other analysts are less certain. Transfers may be “transformative” because they remove negotiating complexities, acknowledged Generate’s Robbins. But “it still takes a lot of work to get a single tax credit investor over the line, whether it is a $100,000 project or a $100 million project,” she added.

However, transferability will be especially valuable for some technologies and investment opportunities, analysts said.

Transferability players and deals

Some renewable energy technologies like utility-scale wind and solar are expected to benefit more and sooner from the new transactions because they are more familiar to the investment community, Segue’s Riester, Reunion’s Lee, AES’s Glazer and others said.

A recent tax credit sale returned $459,000 from an undisclosed buyer for two commercial rooftop solar and storage projects with a combined 537 kWdc capacity and a total cost of $1.5 million, reported Matthew Coleman, CEO of renewables builder Davis Hill Development. The numbers were verified by the James Richards, CEO for transaction intermediary Evergrow.

“A tax equity transaction of that size would be too difficult” because of the extensive legal and other verification by project experts for the complex tax equity partnership agreement that allows investors use of the tax credits, Coleman and Richards agreed. But the reduced due diligence required in the IRA for transferability’s tax credit sale “makes financing feasible,” they added.

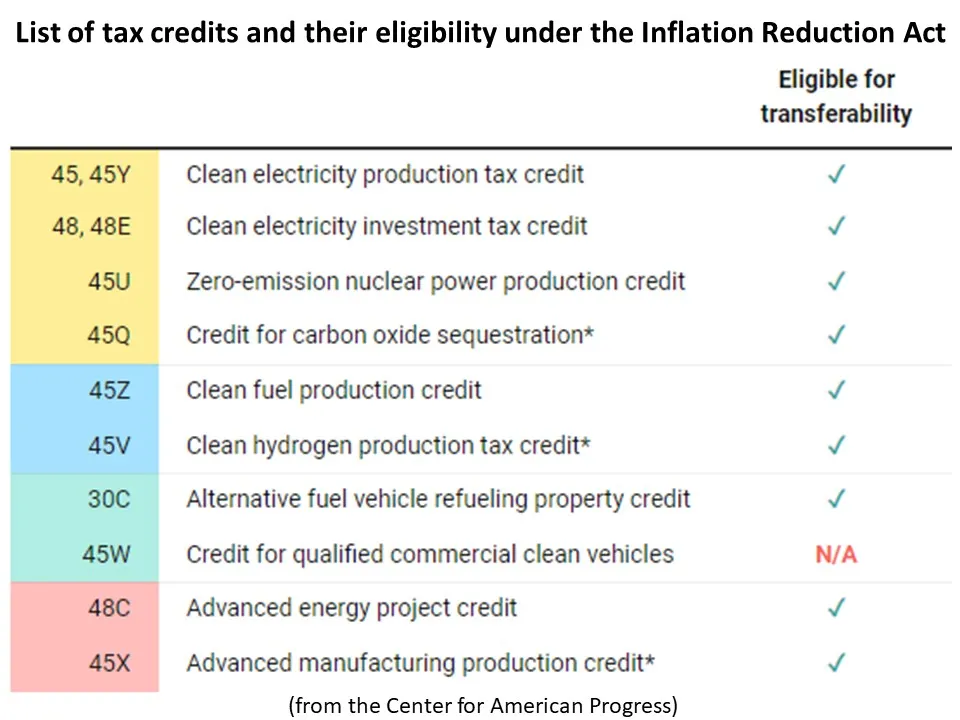

Another transferability use case will be for less proven technologies like carbon capture and clean hydrogen with “too much risk for traditional tax equity investors,” said Generate’s Robbins. But those projects’ capital expenditures “are large enough to justify transferability negotiations and due diligence, even though they are higher risk investments,” she added.

Transferability may also change the financing of merchant utility-scale battery projects, Robbins continued. Their more variable, less predictable revenues will discourage risk averse tax equity investors but allow transferability until merchant storage market risks are better understood, she added.

“Transferability will be absolutely essential” for merchant storage, agreed Jason Burwen, vice president of policy and strategy, for merchant storage provider GridStor.

But to the surprise of many tax credit market-watchers, traditional institutional tax equity investors have been involved in many initial uses of IRA tax credit transferability, instead of the wider investor market that was expected to leap at the opportunity. Generate’s Robbins offered an explanation.

Some equity investors are combining tax credit sales with tax equity partnerships “for technologies like renewable natural gas that are now but were not previously eligible for tax credits,” Robbins said. “The project owner can sell some credits to tax burdened buyers familiar with the technology to reduce the investment debt,” and a tax equity partner could then take limited ownership, and “get the remaining credits and the depreciation value,” she added.

Transferability can also be part of tax equity transactions for technologies with limited risks like solar and wind, Robbins continued. Tax equity investors can monetize their excess tax credits by transferring them to the new buyers like corporate interests coming into the transferability market, she said.

Segue’s Riester disagreed. Tax equity and transferability “will most commonly be used separately” because the hybrid concept tends to make buyers and sellers “skittish,” he said. Financing with transferability will be “faster, with fewer parties, fewer documents, and smaller project finance teams”, he added.

Norton Rose Fulbright’s experience supports Robbins’ idea that many new tax credit sales will be combined with tax equity transactions. The law firm has facilitated the closing of seven tax credit sales through transferability, has 19 in preparation, expects more, and most investors insist on some form of hybrid transaction, Martin said. They want the depreciation deduction available only through tax equity partnerships and not through tax credit sales because it can be worth “up to 14% of a project’s capital cost,” and “that is a lot of money to leave on the table,” he added.

Financial transactions involving tax credit sales through IRA-enabled transferability are only emerging slowly while investors and their legal representatives carefully consider deals with hundreds of millions or billions of dollars at stake.

A $580 million tax credit transfer to Bank of America Securities was part of a recent $1.5 billion equity investment by renewables developer Invenergy and multinational investors CDPQ and Blackstone Infrastructure that closed August 16, according to a release from Norton Rose Fulbright.

On Sept. 27, unregulated renewables developer Avangrid, a subsidiary of the Iberdrola Group, announced the sale of an estimated $100 million of 2023 production tax credits from eight wind projects. Transferability “will allow us to pay down debt and make further capital investments to benefit our customers,” Avangrid CEO Pedro Azagra said in a statement.

On Oct. 2, developer Ashtrom Renewable Energy announced a $435 million equity investment in a Texas solar project that included a $300 million tax credit transfer to an undisclosed “leading U.S.-based institutional entity.”

Utilities are also interested in the IRA’s new mechanism for financing clean energy projects. Transferability can help “ensure we have a diverse mix of energy sources to achieve this ambitious transition in a way that protects reliability,” Duke’s Monroe said. More information on Duke’s potentially groundbreaking auction of tax credits is expected after further Treasury guidance “on IRA implementation is more complete,” he added.

Though some utilities are already buyers and sellers of tax credits, their opportunity "is complicated,” Norton Rose’s Martin said. They face accounting rules imposed by Congress in the 1970s that limit their ownership of renewables and require further specific guidance by the IRS to ensure they can benefit from transferability, he added.

But “if the cost of capital goes up, the cost of energy goes up, power prices go up, and rates go up, and utilities should evaluate how transferability might bring those costs down,” said Reunion’s Lee.

“Many utilities can and should be buyers of tax credits” and some could even handle their own tax credit transactions to “improve their net income,” and lower costs to customers, Segue’s Riester added. “Any and all” tax credit buyers will be needed “to satisfy the absurdly large new supply,” he said.

Two key questions

There are two hurdles transferability still faces, financial and policy analysts say.

Too expensive? The Congressional Joint Committee on Taxation estimated the total tax credit value by 2033 will be worth $663 billion, significantly more the original projection of $369 billion for all the IRA’s climate and energy provisions.

That will, however, depend on how long transferability remains an option, Forbes contributor Marie Sapirie reported June 8. A similar 1981 tax reallocation option was repealed in 1982 after Congress found taxpayers had “responded too enthusiastically,” making it “too expensive” and a threat to taxpayer “respect for and compliance with the tax laws,” Sapirie wrote. “The IRA has the same potential problem,” she added.

A political backlash is concerning, but it is likely to be “reasonably contained,” said Segue’s Riester. Legislative procedure may limit a future Congress’s power to “cancel” the IRA, and the “disproportionate benefits” in red states may make many representatives, though not all, unwilling to vote “against their constituents’ interests,” he added.

Too complex? Transferability advocates are confident transactions will be streamlined, but other analysts are not as certain.

Both tax equity and transferability are relatively complex financial investments that have transaction costs and due diligence complexities that could make scaling transactions difficult, Generate’s Robbins said. Software-enabled platforms that partially automate transactions might, however, “bring new corporate buyers into the market,” and “other possibilities for this marketplace are still emerging,” she added.

Standardization that reduces friction and streamlines transactions “will be challenging initially but participants will move in that direction,” AES’s Glazer agreed.

Digital platforms to streamline transactions are at present “only matching single buyers to single sellers,” Norton Rose’s Martin responded. Their standardized agreements will not replace “due diligence by buyers facing penalties for inaccurate credit valuations,” he added.

But IRA provisions have introduced a “new world” of financing opportunities, and “many new financing structures will emerge to support the many new technologies,” said Generate’s Robbins. “There will be frictions as these new markets develop, but there are a lot of good options,” she added.