Dive Brief:

-

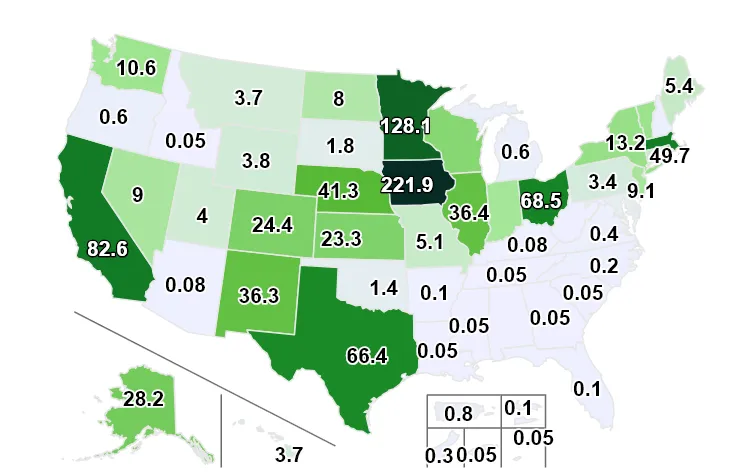

Distributed wind energy appears to be growing in popularity, with 1,994 projects totaling 2.3 MW installed in 2023 compared to 1,745 projects totaling 2.3 MW in 2022 and 1,742 totaling 1.8 MW in 2021, according to the annual Distributed Wind Market Report released Monday by the Pacific Northwest National Laboratory.

-

Distributed wind now generates 1,110 MW, with 89% of new installed capacity intended for on-site use. Historically, distributed wind energy was more likely to be connected to local grid for broader use, according to the report.

-

The increased availability of grants and loans through programs such as the U.S. Department of Agriculture’s Rural Energy for America program likely accounts for much of the increase in installations, according to the report. The Inflation Reduction Act provided these programs with additional funding, and could continue to drive growth in distributed wind installations, said Lindsay Sheridan, the lead author of the report and a wind energy analyst at PNNL.

Dive Insight:

Distributed wind hasn't historically attracted as much attention as rooftop solar, but the Inflation Reduction Act has prompted more U.S. farms and small businesses to give it a second look, according to PNNL.

Agricultural and residential customers have collectively installed 60% of the distributed wind projects built since 2014, according to PNNL's most recent distributed wind report. And they're still a significant player — agricultural customers installed 34% of the nearly 2,000 distributed wind turbines deployed in 2023. But commercial customers accounted for 42% of all distributed wind installed last year, according to PNNL.

This growth can likely be attributed to increased funding available through programs such as the Rural Energy for America program, which provides grants and loan financing to agricultural producers and rural small businesses to install renewable energy systems or energy efficiency upgrades, Sheridan said. The IRA funded 88% of REAP awards issued in 2023, according to the Distributed Wind Market Report. PNNL has also seen distributed wind installation increase in the past when new funding became available, Sheridan said.

Distributed wind development has been impacted by the limited availability of suitable turbines, according to PNNL. GE has been the only consistent U.S.-based provider of turbines suitable to distributed wind projects for the past ten years, according to the report.

But a number of new manufacturers appear poised to enter the market. Ryse Energy purchased U.S.-based Primus Wind Power in 2023 and launched a new manufacturing facility in Texas, and Wind Resource purchased the Skystream turbine model line, signaling an interest in entering the U.S. distributed wind market, according to PNNL.

With additional incentives still coming online, there appears to be even more potential for distributed wind growth in 2024 and beyond, Sheridan said. The Rural and Agricultural Income & Savings from Renewable Energy initiative, for example, will support both the commercialization of distributed wind technologies and the development of business models that will help farmers earn revenue from distributed wind turbines, she said.

And that growth could be significant, Sheridan said. While distributed wind shares some of the same limitations as utility-scale wind in that it benefits from installation at a location with good wind resources, distributed wind projects tend to be somewhat more flexible and can be customized to suit smaller spaces, she said.

“We're not yet close to any distributed wind deployment limit,” she said.